- Ag Market Insights

- Posts

- As Usual – Grain Market Volatility Continues: Here is Your Daily Update

As Usual – Grain Market Volatility Continues: Here is Your Daily Update

Market Insights and Forecasts - September 16

Ag Market Insights is dedicated to bringing you timely information to help you consistently get the most money for your crops. Our team painstakingly goes through mountains of information and data and distills insights into a format that you can consume in a few minutes.

Prices as of September 12th, 2024 – 20:00CDT

In this edition:

Harvest Headlines: Corn and wheat bump up, while soybean slide a little.

Market Actions: No new triggers.

Crop Supply and Demand: Starting to see some gaps open up between supply and demand. The charts below detail these gaps.

The information provided in this newsletter is for informational purposes only and should not be considered financial advice. We recommend consulting with a commodities broker and financial advisor before making any commodities decisions.

Harvest Headlines

Corn and wheat markets saw upward momentum, driven by strong export demand and global supply concerns. In contrast, soybeans have experienced a downward trend due to weakening demand and expectations of larger global supplies. The ongoing weather conditions and geopolitical factors continue to play a significant role in shaping market movements across these commodities.

The September WASDE report didn’t bring many surprises. U.S. corn yields might continue to rise, while there’s still uncertainty around soybean yields, with both farmers and the USDA unsure of the final numbers. Since both crops are projected to reach record highs, no one will make bold predictions until the combines start harvesting and reveal the true outcome in the Midwest.

Corn Market Overview

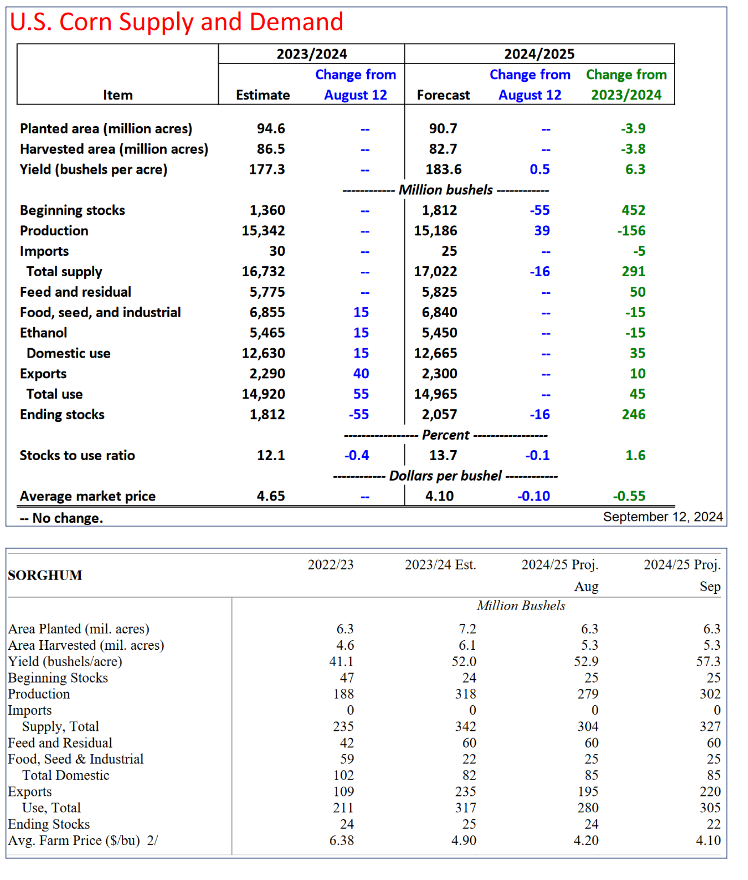

U.S. corn production for the 2024/25 season is projected at 15.2 billion bushels, an increase of 39 million bushels from the previous month. The harvested area remains steady at 82.7 million acres, while total corn usage in the U.S. holds at 15.0 billion bushels. With a drop in supply and no change in usage, ending stocks are reduced by 16 million bushels, now at 2.1 billion. The season-average corn price received by farmers is lowered by 10 cents, bringing it to $4.10 per bushel.

Corn futures saw an increase due to stronger-than-expected export sales and robust domestic demand.

Ongoing dryness in key producing regions has raised concerns about yield potential, supporting prices.

Brazil's corn exports have continued at a strong pace, adding competition to U.S. exports.

Ukraine's reduced grain shipments, amid the conflict with Russia, have added pressure on global corn availability.

Corn yield prospects in the U.S. are uncertain, with some areas reporting better-than-expected results, while others remain below average.

U.S. ethanol production remains steady, supporting domestic corn demand.

Soybean Market Overview

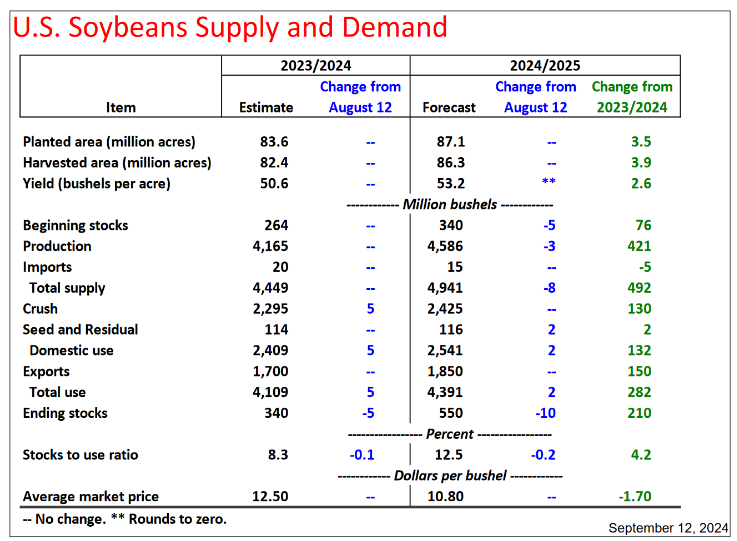

The U.S. soybean yield for the 2024/25 season remains at 53.2 bushels per acre, unchanged from August. However, most states saw adjustments, with Ohio experiencing a significant decrease. Meanwhile, Iowa is now projected to match its record yield from 2021.

Soybean futures slid as Brazil and Argentina are expected to produce bumper crops, increasing global supplies.

China, a major importer of U.S. soybeans, has recently scaled back its purchases, adding pressure to prices.

Concerns over weak domestic demand for soybean meal and oil have contributed to the bearish sentiment.

The strong dollar has also weighed on U.S. soybean competitiveness in international markets.

Favorable weather in South America has improved the outlook for the upcoming planting season, further pressuring U.S. prices.

U.S. crush margins have tightened, leading to reduced processing rates and lower demand for soybeans.

Wheat Market Overview

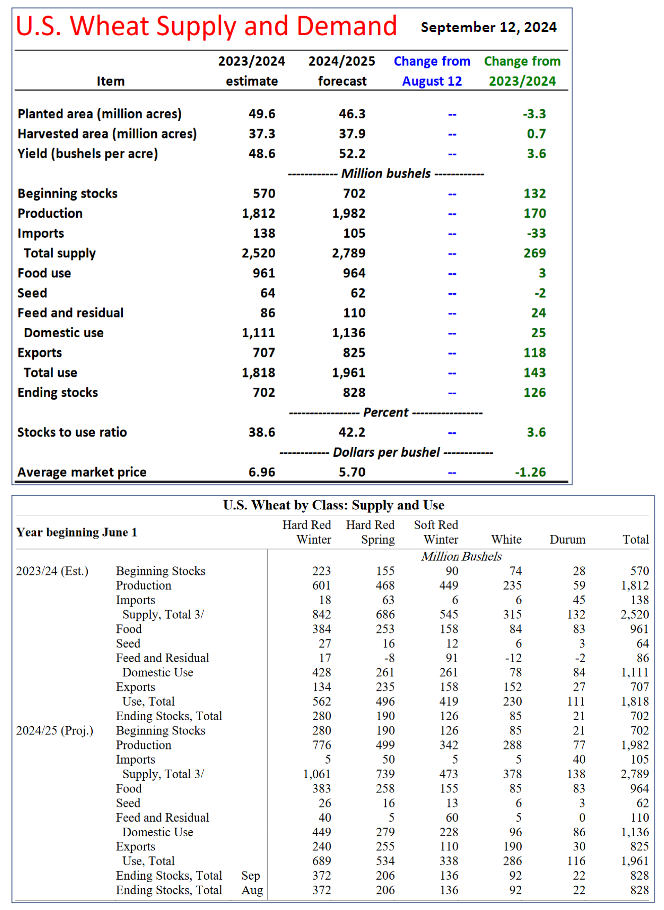

The USDA made no adjustments to the U.S. wheat balance sheet or to individual wheat classes. As a result, U.S. wheat ending stocks remain at 828 million bushels, with 372 million in Hard Red Winter, 136 million in Soft Red Winter, 206 million in Spring, 92 million in White, and 22 million in Durum wheat. The USDA also left the average farm price unchanged at $5.70 per bushel.

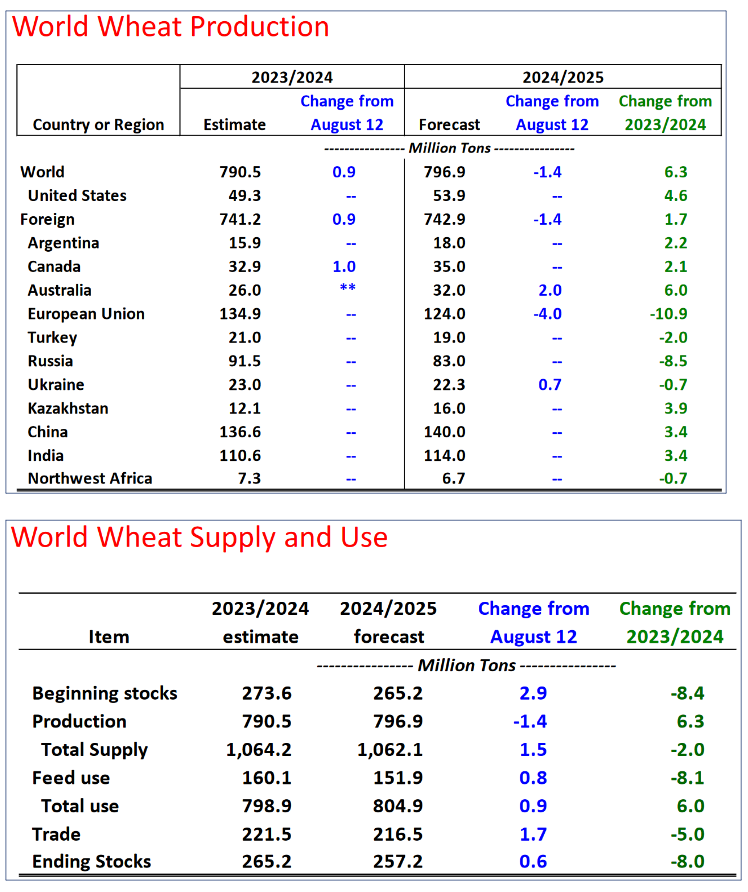

Global wheat ending stocks for the 2024/25 season saw a slight increase from last month, contrary to the average trade estimate, which expected a reduction of over 1 MMT. The USDA raised beginning stocks by 2.89 MMT, largely due to a 2.75 MMT increase from Canada, with minor reductions in Australia and the EU. Global wheat production for 2024/25 was cut by 1.4 MMT. The EU's wheat crop estimate was lowered by 4 MMT to 124 MMT, though this was partially offset by a 2.5 MMT reduction in exports. Ukraine's wheat exports for 2024/25 were raised by 1 MMT to 15 MMT, still below last year's 18.6 MMT.

Wheat futures rallied on continued concerns over Black Sea region exports, particularly from Ukraine, which are disrupted by the ongoing conflict.

Dry weather conditions in Australia and parts of Canada have reduced global wheat production forecasts.

Strong demand for U.S. wheat, particularly from Asia and the Middle East, has provided support to prices.

The USDA's recent report showed tighter-than-expected wheat stocks, adding to bullish sentiment in the market.

Ongoing inflation in input costs, including fertilizers, continues to impact production margins for wheat farmers globally.

Supply and Demand

Extended Commentary

As we navigate the current grain markets, volatility remains the key theme, with corn and wheat prices gaining some ground while soybeans continue their slide. The latest WASDE report provided minimal surprises but highlighted ongoing trends shaping market movements in the coming weeks.

Corn futures have strengthened due to increased export sales and steady domestic demand, even as the market braces for record-high U.S. production. The USDA projects the 2024/25 U.S. corn production at 15.2 billion bushels, a slight increase from the previous month, with yields expected to reach 183.6 bushels per acre. However, global dynamics are creating a mixed picture. Brazil's corn exports continue steadily, intensifying competition for U.S. exports. Additionally, Ukraine's reduced grain shipments amid ongoing geopolitical tensions have tightened global supply. U.S. ethanol production remains steady, supporting domestic demand for corn, but concerns persist over the impact of dryness in key producing regions. As a result, prices hold firm, though uncertainty over yield outcomes and export competition may keep the market volatile.

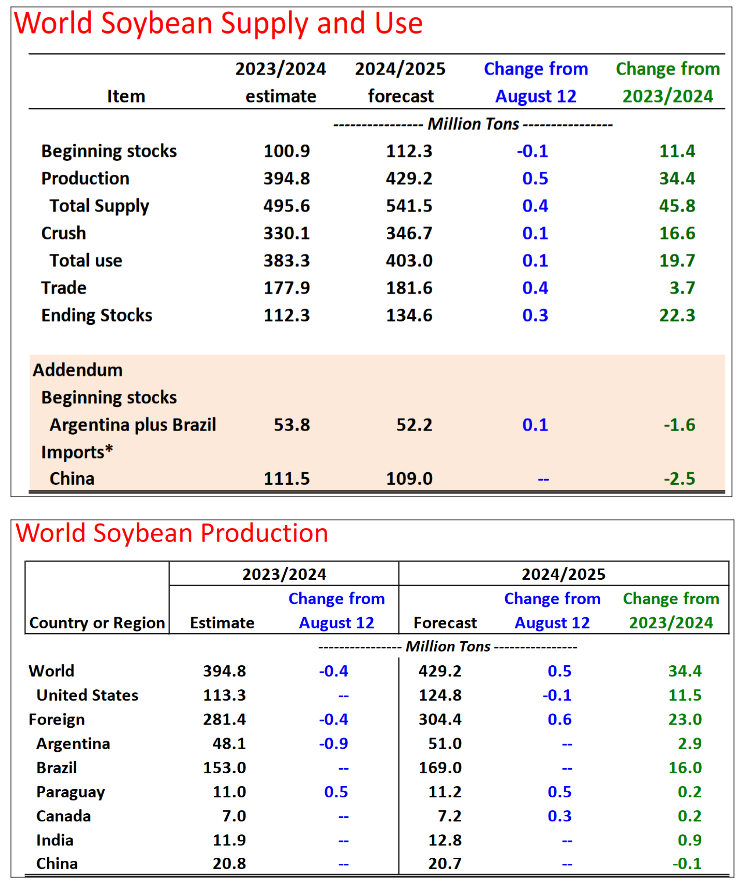

Soybean prices have remained under pressure, reflecting concerns over weakening demand and expectations of bumper crops in Brazil and Argentina. The USDA's soybean yield projection remains at 53.2 bushels per acre for the 2024/25 season, while Brazil and Argentina are gearing up for potentially record-high harvests, adding to global supply concerns. China's recent reduction in U.S. soybean purchases has further weighed on the market, compounded by a strong dollar, which is affecting the competitiveness of U.S. soybeans internationally. Additionally, tightening U.S. crush margins has slowed processing rates, reducing domestic soybean demand. While weather conditions in South America are currently favorable, further pressure on prices could arise if planting proceeds smoothly. The market will continue to monitor demand signals, particularly from China, and any changes in global supply dynamics.

Wheat markets are also experiencing volatility, with prices responding to a mix of global supply concerns and geopolitical factors. While the USDA left the U.S. wheat balance sheet unchanged, global ending stocks for the 2024/25 season have slightly increased due to higher beginning stocks, mainly from Canada. Global production, however, was cut by 1.4 MMT, with the EU's wheat crop estimate lowered significantly. Despite these adjustments, wheat faces headwinds from competitive Russian exports and robust global supply. The ongoing conflict in Ukraine disrupts exports from the Black Sea region, adding uncertainty to global wheat availability. Meanwhile, dry weather conditions in Australia and Canada contribute to concerns about future production levels. Input cost inflation, including higher fertilizer prices, remains challenging for wheat farmers worldwide, potentially impacting production margins and future planting decisions.

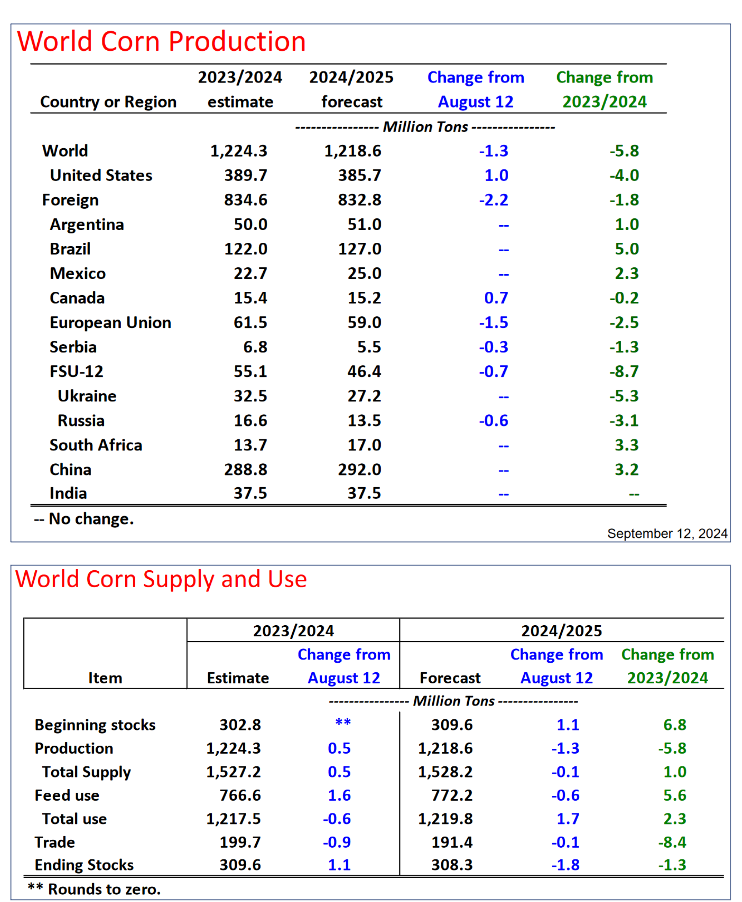

The USDA's latest data reveals growing gaps between supply and demand across several vital commodities. For corn, the U.S. ending stocks for 2024/25 are forecasted at 2.1 billion bushels, while the global supply outlook remains tight, with projected world corn production declining slightly from the previous year. For soybeans, ending stocks are expected to increase to 550 million bushels, reflecting a more comfortable supply situation, though this could shift depending on harvest outcomes and export demand. The global wheat supply is forecasted at 796.9 million tons for 2024/25, with ending stocks at 257.2 million tons, suggesting that while supplies are ample, market volatility remains due to ongoing geopolitical and weather-related factors.

As the harvest season progresses, market participants closely monitor yield reports and global supply dynamics. The current environment, marked by strong export demand for corn and wheat and weaker soybean prices due to global supply expectations, underscores the ongoing volatility in grain markets. Supply and demand gaps are beginning to emerge, and geopolitical factors and weather conditions in key growing regions will continue to play a crucial role in shaping market direction. Traders and producers should remain vigilant as the landscape evolves, with potential price shifts on the horizon as the true scope of this year's harvest comes into view.