- Ag Market Insights

- Posts

- Grain Markets Slip Amid Harvest Pressure and Supply Chain Concerns

Grain Markets Slip Amid Harvest Pressure and Supply Chain Concerns

Market Insights and Forecasts - September 23

Ag Market Insights is dedicated to bringing you timely information to help you consistently get the most money for your crops. Our team painstakingly goes through mountains of information and data and distills insights into a format that you can consume in a few minutes.

In this edition:

Harvest Headlines: Relatively movement or significant events.

Market Actions: No new market triggers. An unexpected drop in projected supply or a rise in demand could prompt managed funds to cover more of their large short positions, driving prices higher. However, a sustained rally for corn, soybeans, or wheat is unlikely to occur before the harvest is completed.

One Week Corn Technical Analysis: The technical analysis of corn is slightly more bearish than last week, but it is leveling off and dovetailing with our AI fundamental models’ predictions of prices leveling off and then slowly creeping up.

Market Overview

Grain markets ended mostly lower this week as harvest pressure continues to weigh on prices. Despite some supportive demand news, the general sentiment remains cautious amid the ongoing harvest season and concerns over global supply chain disruptions. Corn and soybeans both faced downward pressure, while wheat showed some resilience, supported by global supply issues. The overall market is adjusting to new crop data and export dynamics.

The information provided in this newsletter is for informational purposes only and should not be considered financial advice. We recommend consulting with a commodities broker and financial advisor before making any commodities decisions.

Prices as of September 22nd, 2024 – 20:00CDT

Harvest Headlines

Corn Price Events

Harvest Pressure: Corn prices declined as the U.S. harvest progresses, adding to the supply and pressuring futures.

Demand Uncertainty: Weak ethanol demand and lackluster export sales have contributed to a bearish outlook.

Export Sales: Weekly export sales were below expectations, with stiff competition from South American producers.

USDA Reports: The USDA's recent report indicated higher-than-expected corn stocks, adding to the downward pressure on prices.

Weather Conditions: Favorable weather in the Midwest has facilitated rapid harvesting, leading to increased supply.

Brazilian Crop: Expectations of a record Brazilian corn crop are adding to the global supply concerns.

Since their peak in early July, managed funds have reduced more than 200,000 net short contracts, even though the corn market has seen only a modest rally. According to Friday's Commitment of Traders report, it is anticipated that the funds will have fewer than 100,000 net short contracts, marking their smallest net short position of the year as the harvest begins to pick up.

China Demand: Uncertainty over Chinese demand for U.S. corn has also contributed to the bearish sentiment.

Soybean Price Events

Harvest Impact: Soybean futures were lower due to harvest pressure, as farmers deliver new crop supplies to the market.

China’s Purchases: Despite recent purchases, overall Chinese demand is seen as inconsistent, affecting price stability.

Crush Margins: Declining crush margins in the U.S. have raised concerns about domestic demand.

Although October grain options are part of a serial option, they expired today, and prices tend to move toward areas with substantial open interest on expiration day. At the beginning of the session, there was a combined open interest of nearly 16,000 put options at the 1000 and 1010 levels. Since the market closed at 1012, those put options ended up expiring worthless.

South American Competition: The ongoing Brazilian planting season and favorable weather forecasts could lead to strong competition in the coming months.

Biofuel Demand: Concerns over policy changes affecting biofuel demand are also weighing on soybean prices.

Export Pace: Export inspections are trailing last year's pace, signaling potential challenges in meeting USDA projections.

Global Supply Chain: Ongoing disruptions in global supply chains are creating logistical challenges, impacting exports.

Wheat Price Events

Global Supply Concerns: Wheat prices found support due to ongoing concerns over global supply disruptions, particularly from the Black Sea region.

U.S. Exports: Stronger-than-expected U.S. wheat exports have provided some support to the market.

Ukraine Exports: Despite the conflict, Ukraine remains a key player in the global wheat market, but export logistics remain uncertain.

Planting Progress: Winter wheat planting in the U.S. is progressing well, with favorable weather conditions aiding farmers.

The Belgian trade association Coceral has revised its EU grain production forecast down to 280.3 million metric tons, a decrease from its June projection of 296 million metric tons. This includes 126 million metric tons of soft wheat, down from the previous estimate of 134.5 million metric tons in June.

Australia’s Crop: Forecasts of a bumper wheat crop in Australia could increase global supplies, pressuring prices in the long term.

Currency Impact: A stronger U.S. dollar is making U.S. wheat less competitive on the global market.

Weather Factors: Dry conditions in key growing regions like Argentina and Canada are also being closely watched by the market.

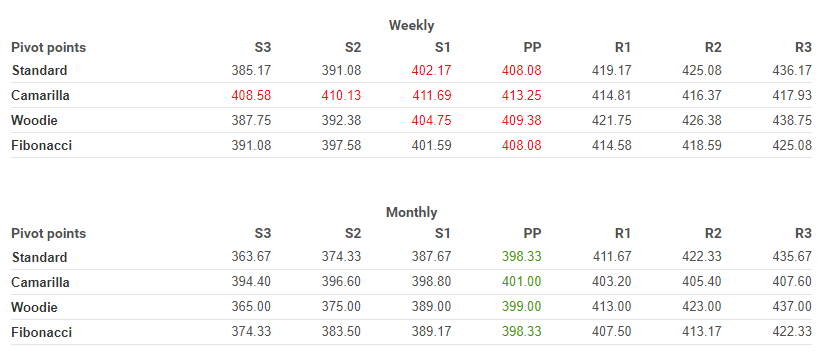

Corn – Weekly Technical Analysis

9/16/2024-20:00CDT

This analysis presents a composite analysis that we have developed to evaluate technical indicators. We have back tested this model with thousands of scenarios. The back testing has proven the model to be accurate 65.6% of the time. This is significantly better than other technical analysis techniques. This is a weekly analysis that analyzes if there are any changes in trends.

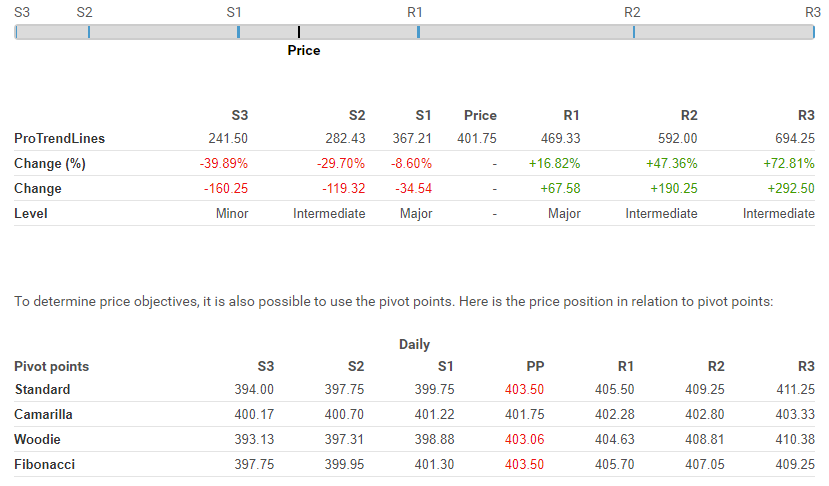

This week’s technical analysis of corn is in line with last week’s analysis. The bearish trend is currently strong for CORN. Traders may consider trading only short positions (for sale) as long as the price remains well below 435.67 USD. The next support located at 367.21 USD is the next bearish objective to target. A bearish break of this support would revive the bearish momentum. The bearish movement could then continue towards the next support located at 363.67 USD. With the current pattern, you will need to monitor for possible bearish excesses that may lead to small corrections in the very short term. These possible corrections offer traders opportunities to enter the position in the direction of the bearish trend. Trying to profit from the purchase of these possible corrections may seem risky.

The force of this analysis is 6.6, which is moderately strong but not at level 8 or above. Wheat has been on a downward trend, but that trend seems to be leveling off. This aligns with out AI fundamental models that suggest that wheat are going to be volatile but will level off and gradually increase.

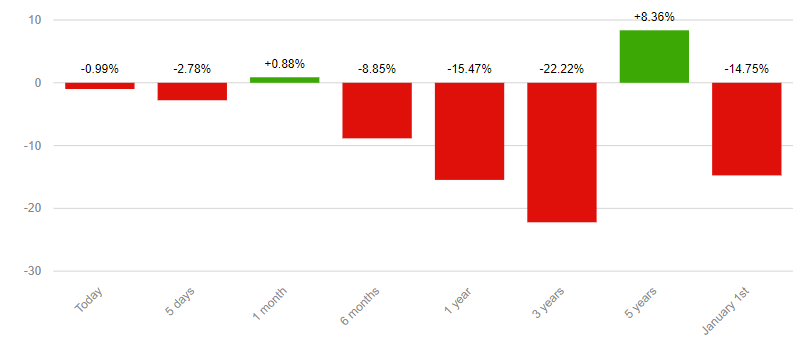

The price is lower by -2.78% over the 5 days and has been traded over the last 5 days between 401.50 USD and 415.00 USD. This implies that the 5-day price is +0.06% from its lowest point and -3.19% from its highest point.

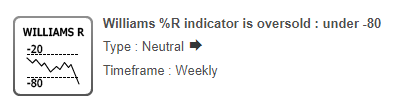

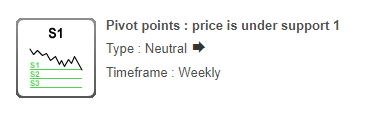

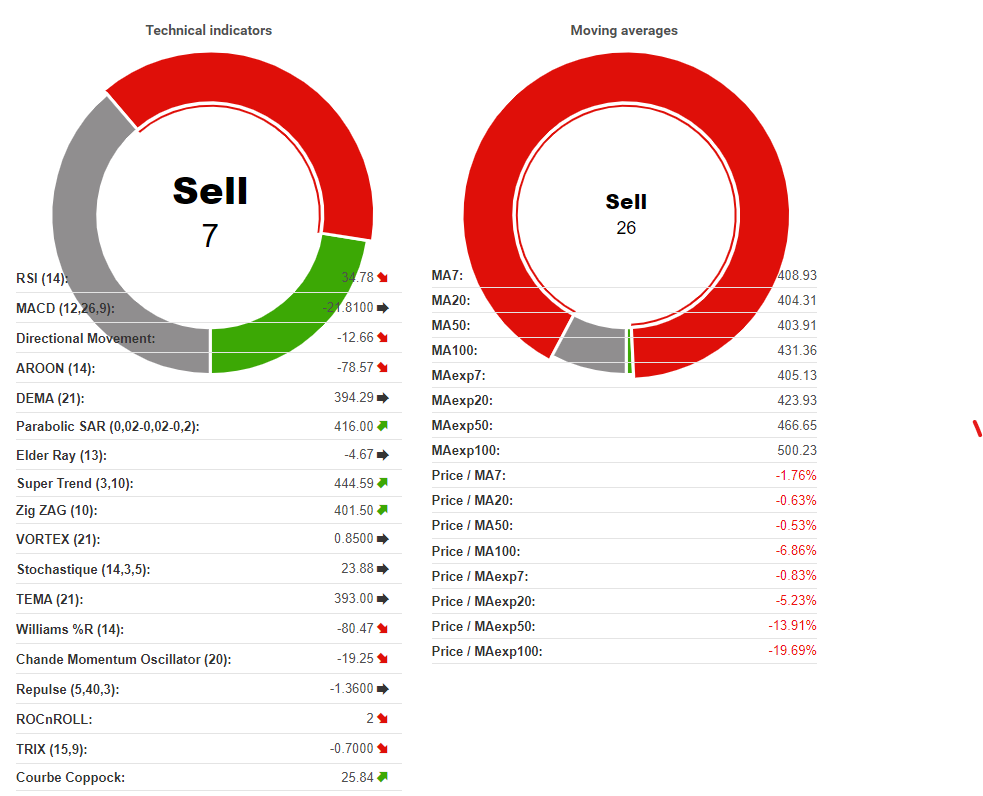

The Central Indicators scanner currently detects an excess:

Extended Commentary

The grain markets continue to face mounting pressure as the harvest season picks up, and corn prices have notably declined. Weak export sales and favorable harvest conditions in the Midwest have contributed to a bearish outlook for corn. Despite some concerns over drought conditions in 26% of U.S. corn acres, the accelerated pace of harvesting has introduced more supply into the market, driving prices lower. Competition from a potentially record-breaking Brazilian corn crop adds to global supply concerns, likely limiting any short-term price recovery.

Soybean markets also saw downward movement, influenced by the harvest pressure and inconsistent Chinese demand. While Chinese purchases had initially provided some support, the overall regional demand remains uncertain, contributing to the lack of price stability. Additionally, declining U.S. crush margins and stronger-than-expected competition from South American producers have added to the bearish sentiment. With biofuel demand concerns and logistical challenges from global supply chain disruptions, soybean prices will likely remain under pressure in the coming weeks.

Wheat prices fared slightly better, bolstered by concerns over global supply disruptions. However, the ongoing conflict in Ukraine and logistical issues continue to create uncertainty in the market. Wheat exports from the U.S. have exceeded expectations, providing some price support. Nevertheless, the global wheat outlook remains cautious as forecasts from critical regions, such as Australia and the EU, suggest higher-than-anticipated production, which could increase global supplies and weigh on prices in the longer term.

Technically, the corn market continues to exhibit a solid bearish trend, with indicators pointing to further downside potential. Prices are hovering around crucial support levels, and the bearish momentum is unlikely to ease unless there is a significant shift in market dynamics, such as a reduction in global supplies or a sudden spike in demand. The current harvest pressure and export competition will likely keep prices subdued soon.

Looking ahead, volatility remains a key concern across all grain markets. While wheat may experience upward momentum due to supply uncertainties, corn and soybean prices are expected to remain bearish as the harvest progresses and global competition intensifies. Traders should remain cautious, keeping a close eye on export data and weather conditions in key producing regions, as these factors will heavily influence market direction in the coming weeks.